How are you protected if you become unable to work due to illness or accident? Income protection insurance protects you against loss of income and gaps in your social insurance contributions.

Benefits

Protects you against loss of earnings

Individual choice of pension amounts

Choice of waiting period

Tax advantage under pillar 3a

Overall rating

4.3/5

79.617

of

79.617

reviews

How income protection insurance works

We will pay you a pension if you experience loss of earning capacity. A premium exemption is always included, too. Speak with one of our experts for personalised advice on which add-ons would best meet your needs, or simply take out online income protection insurance in a ready-made package here.

Your benefits

Unable to work: What now?

So you can maintain your standard of living.

Loss of earning capacity due to illness or accident

Individual choice of amount of pension

Tax advantages with premiums saved in pillar 3

Including premium exemption: Premiums covered in emergencies

For an analysis of your situation and personalised quotes.

Coverage types in detail

Risk protection

Pension

Premium exemption

In brief

Covers gaps in social insurance

Protect against illness, the biggest risk

Combine illness and accident

Protect yourself from life’s greatest risks You decide if you only insure against the risk of illness, which lowers your premiums. Or you can decide to insure against both illness and accident.

The most common cause of loss of earning capacity Around 80% of those who experience loss of earning capacity do so due to illness. But regular social insurance payments often do not cover enough of your costs if you are ill. Usually, you receive only between 60 and 70% of your former salary. This is in sharp contrast to an accident, where you will receive up to 90% of your former salary. That’s why we offer you the option of cheaper premiums that only insure against illness.

Pension to maintain your standard of living Income protection insurance protects your standard of living in the event that you become unable to work due to an accident or illness. We will then pay you a quarterly pension, protecting your personal income.

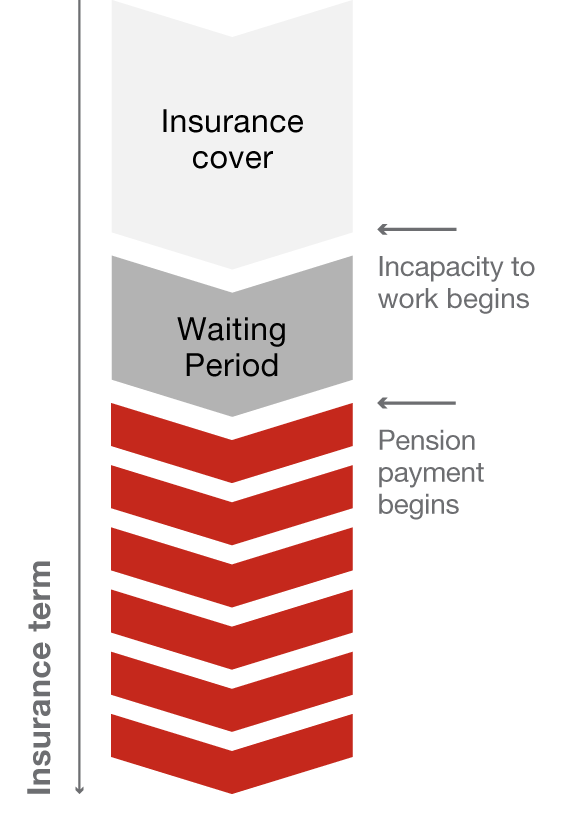

Choice of pension amounts and waiting periods The legal waiting period is 720 days. With us, you can reduce this period down to just 30 days. You’ll also be able to choose the pension amount to suit your personal needs.

In brief

Continuation of premium payments

Paid after an agreed period

Automatically covered

Well protected despite loss of earnings If you lose your income because you are unable to work due to illness or an accident, we will continue paying your premiums. This removes a major financial burden and guarantees that you will remain insured.

Which pension solution is right for your personal life circumstances? With our pension calculator, you can analyse any gaps in your pension coverage directly online in just a few minutes. Try it now and start your analysis. Free of charge, with no strings attached.

Income protection insurance offers protection for everyone – regardless of whether self-employed or not. This is because time off work due to illness can create big gaps in your social insurance contributions. If you are unable or unwilling to dip into your savings to fill these gaps, income protection insurance will be a good choice for you.

We recommend taking out income protection insurance as early as possible. This is because you will no longer qualify for the policy once you become incapacitated in some way, or will only be able to do so subject to much stricter conditions. Plus, the age you are when taking it out also affects your premiums: the earlier you take it out, the lower the premiums.

The cost of the premiums depends on your personal risk profile. It also depends on the pension amount and the waiting period you choose. The smaller the pension and the longer the waiting period, the lower the cost of your income protection insurance will be.

In a nutshell, income protection insurance protects you if you lose your capacity to engage in any gainful employment whatsoever. An occupational disability, by contrast, would mean losing your ability to perform a specific job. In this case, it would be possible and reasonable for you retrain for another job.

Income protection insurance covers you if you become totally or partially disabled and unable to work. In this case, it will cover the income you have lost. However, you could also lose your earnings for reasons that are not health-related, such as leaving or losing your job, as a result of which you might be left without an income. This is not the same as a disability or becoming unable to work.

You can pay your income protection insurance premiums into your private pension, i.e. pillar 3a or 3b. This way, you are both protecting yourself from risks and saving for your retirement at the same time. This savings component is optional. If you would like to add it, please speak to one of our advisors.

Yes, they will be tax-deductible if you take out income protection insurance as part of a pillar 3a or 3b account. With a tied pension, the premium will count as a pillar 3a payment and can be deducted from your taxable income.

Yes, any payments you receive from your income protection insurance are subject to tax in the same way as a regular income.

You can pay your premiums monthly, quarterly, six-monthly or annually. You can easily and conveniently do so via direct debit, for example. Finance the premiums via an interest-bearing premium deposit account and benefit from attractive interest rates.

You can cancel your policy as set out in the terms and conditions. Normally, this would be annually when the relevant insurance year runs out. This date will be stated in your policy document. Please note that, although you will be able to cancel your policy, you will not be able to redeem it. This means that you will not get any money back if you cancel it.

Our expert advisors will help you to find the perfect insurance coverage in every phase of life. If you have a specific question about an insurance policy, we will answer it quickly and expertly.

If you would like a better understanding of your overall situation, we will work with you to analyse your needs and goals. We will recommend the right solutions for your insurance coverage and your financial security.

The advice is free of charge, with no strings attached. You choose the time and place.

Contact

Contact

Find an agency

Find an agency

Close

Close